Over the past year, the team at EAS has spent a lot of time deep diving into agricultural GHG accounting frameworks — building methods for inventories, insetting programmes, product emissions intensity reporting, and supply-chain decarbonisation strategies for a range of clients.

One recurring request seems simple enough on the surface:

“Can’t we just create one method that does all the reporting we need?”

The short answer is: not really.

Not because the science is impossible, but because modern carbon accounting is increasingly trying to make one number do too many different things at once.

Companies want inventories that are scientifically defensible. Investors want comparability. Sustainability teams want flexibility to recognise supplier engagement and insetting. Farmers need systems that are practical that can lead to ‘rewards’. Regulators want claims that are not misleading.

The problem is that these objectives do not always align.

That tension in the Agricultural sector has become particularly interesting in light of two recent papers by Michael Brander from the University of Edinburgh and Michael Gillenwater from the GHG Institute, both of which critique the logic of market-based accounting in Scope 2 emissions.

While these papers focus on electricity accounting, their implications for agricultural Scope 3 accounting may be even more significant. This is particularly relevant given the GHG Protocol’s Actions and Market Instruments (AMI) Standard is under development, to expand the concept of market-based accounting, currently limited only to Scope 2, to other Scopes.

The Scope 2 debate in simple terms

“Both papers question whether companies should be able to report lower emissions simply because they have financially supported a lower-emissions product (in Scope 2, this always refers to purchased electricity). Demonstration of financial support could be through contractual arrangements with renewable electricity suppliers, or purchasing of Renewable Energy Certificates (RECs) or Energy Attribute Certificates (EACs).

Brander’s argument is fundamentally about physical reality versus contractual allocation.

A company connected to a fossil-heavy grid may purchase renewable certificates and then report near-zero Scope 2 emissions under market-based accounting. But the company still physically consumes electricity from the broader grid mix.

His critique is that contractual ownership is not the same thing as physical causation.

The GHG Institute paper takes the argument further. It suggests the issue is not simply poor Scope 2 design, but the broader mixing of two different accounting questions:

- What emissions physically occurred?

- What climate actions or market interventions did the company support?

The paper argues these may need to be reported separately rather than combined into a single emissions figure.

That sounds like a technical accounting debate. But once you apply the same logic to Scope 3 in the agricultural sector things become much more uncomfortable.

Agriculture may have the same problem — only messier

At first glance, the analogy seems obvious.

In electricity:

- a company physically consumes average grid electricity,

- but reports lower emissions through certificates.

In agriculture:

- a company physically procures from a mixed commodity pool,

- but may report lower emissions through:

- supplier programmes,

- inset claims,

- mass-balance sourcing,

- sustainable commodity certificates,

- jurisdictional approaches,

- or portfolio-average emission factors.

In both cases, emissions reported may not correspond directly to the physical product consumed.

That creates a parallel with the same critique now emerging in Scope 2: contractual allocation does not necessarily equal physical attribution.

But agriculture is structurally far more complicated than electricity.

Electricity systems operate with relatively consistent physics, measurable grids, known generation nodes, and increasingly sophisticated tracking systems.

Agricultural supply chains look very different.

They consist of fragmented global supply chains, rely on sparse and uncertain farm data from millions of diffuse producers working in a biologically variable and ever changeable growing environment.

This is where the challenge becomes real.

Most agricultural systems simply do not support perfect physical traceability.

Grain is mixed in silos. Milk pools across regions. Livestock from multiple farms enter shared processing systems. Commodities pass through multiple intermediaries long before reaching a downstream buyer.

If strict physical traceability became mandatory, many existing agricultural mitigation programmes would struggle to function at scale; noting the Value Change Initiative work in this area.

The uncomfortable trade-off

This creates a dilemma that the agricultural sector has not fully resolved.

On one side:

- stricter attribution rules improve scientific defensibility and claims integrity.

On the other:

- flexible allocation systems may be the only practical way to finance mitigation across highly fragmented agricultural systems.

That tension sits at the centre of many current debates around:

- insetting,

- book-and-claim systems,

- sustainable commodity programmes,

- and Scope 3 reduction claims.

And this is where the Scope 2 debate suddenly becomes highly relevant.

If critics argue that electricity certificates cannot credibly substitute for physical electricity flows, what does that imply for agricultural Scope 3 claims where physical traceability is often even weaker?

There is no easy answer.

Why this matters for insetting

This issue becomes particularly important when discussing agricultural insetting, where food and agribusinesses invest in reducing or removing greenhouse gas emissions directly within their own supply chains, rather than purchasing external carbon offsets.

Many inset systems effectively assume that a company can claim mitigation outcomes occurring somewhere within its supply shed (i.e. localized sourcing regions used by brands to track and pool emission reductions when exact farm origins are unknown), even if those reductions are not directly linked to the physical commodities it purchased.

That creates clear parallels with Scope 2 market based accounting.

Critics would argue these systems risk:

- weak causality,

- double counting,

- and claims that drift too far from physical emissions reality.

Supporters would argue something equally important:

agriculture is unlikely to decarbonise at scale without systems like these.

And that may be true.

Unlike electricity markets, agricultural supply chains often lack the infrastructure, traceability, and monitoring capability needed to build perfectly attributable inventories across global commodity systems.

So the sector may be forced to accept some level of abstraction.

The real question is whether we are being sufficiently transparent about what those abstractions actually represent.

Maybe Scope 3 is trying to do too many things at once

The deeper issue exposed by these debates is surprisingly simple:

What is Scope 3 actually for?

Is it intended to:

- describe physical emissions responsibility?,

- incentivise mitigation?,

- reward climate finance?,

- drive supplier engagement?,

- estimate consequential impacts?,

- or support transition planning?

Right now, many systems attempt to do all of these simultaneously.

That is where the internal tension starts to emerge.

An inventory is supposed to answer:

“What emissions are associated with this value chain?”

A mitigation programme is trying to answer:

“What actions did the company help drive?”

A climate finance mechanism asks:

“What decarbonisation did the company enable?”

These are related questions, but they are not the same.

Current agricultural Scope 3 systems often compress them into a single emissions number.

That may be where the accounting starts becoming conceptually unstable.

The idea of multi-statement reporting

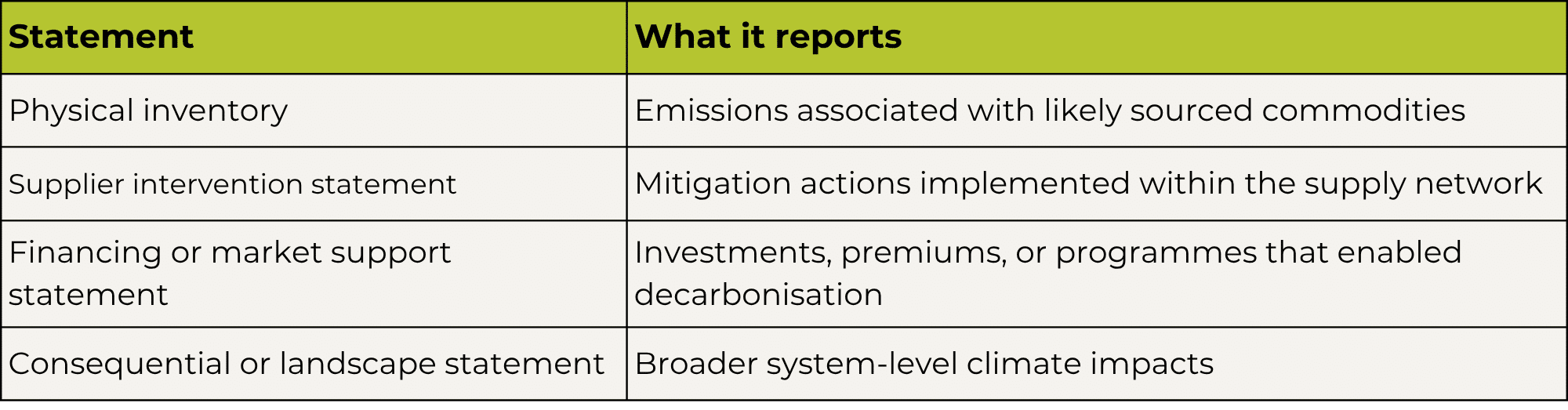

One of the more interesting ideas emerging from the GHG Institute paper is the concept of “multi-statement reporting”.

Instead of forcing one number to carry every meaning, companies could separately disclose:

- physical inventories,

- supplier mitigation activity,

- market-based interventions,

- and consequential climate impacts (which is already required for Scope 2 under the GHG Protocol).

For agriculture, that might look something like this:

This does not eliminate insetting, certificates, or supplier programmes. But it changes what they mean.

Instead of saying:

“Our purchased commodities have lower emissions,”

the claim may become:

“Our company helped drive mitigation within the supply system.”

That is a subtle but potentially profound shift.

Why this debate is becoming unavoidable

This is no longer just an academic accounting discussion.

The outcome affects:

- how food companies communicate net-zero progress,

- how agricultural climate claims are regulated,

- how farmers are rewarded for mitigation,

- and how investors interpret supply-chain decarbonisation.

The pressure is increasing from all directions.

Investors want robust inventories. Regulators are scrutinising green claims more aggressively. Companies still need scalable mechanisms to support mitigation in diffuse agricultural systems. Farmers need pathways that are practical, affordable, and inclusive.

The challenge is that agricultural decarbonisation may not scale without some form of abstract allocation or market-based incentive system.

Yet the further these systems drift from physical attribution, the greater the risk that Scope 3 inventories become disconnected from what they are supposedly measuring.

Agriculture may ultimately force the carbon accounting world to confront a difficult reality:

we may not be able to build a single number that simultaneously represents physical emissions, rewards mitigation, attracts finance, supports farmer participation, and satisfies claims integrity.

If that is true, then the future of Scope 3 accounting may not be about finding the perfect allocation factor or certificate design.

It may be about learning how to tell several different — but transparent — stories at once.