Overview

This guide explains how New Zealand’s Nationally Determined Contribution (NDC) under the Paris Agreement interacts with the Voluntary Carbon Market (VCM) and why double counting is an important issue for both governments and voluntary buyers.

- The NDC is New Zealand’s official emissions-reduction commitment and governs how the country accounts for GHG reductions.

- The VCM is a separate, private-market system allowing organisations and individuals to purchase carbon credits for voluntary climate claims.

- Although both systems generate emission reduction/removal credits, they operate under different rules, governance structures, and end uses.

- Article 6 of the Paris Agreement provides the framework for international carbon credit transfers between countries.

- Double counting occurs when the same reduction or removal is used more than once. Article 6 prevents double counting between countries, but corporate voluntary claims fall outside UNFCCC accounting rules.

- Understanding these distinctions helps project developers, organisations, and buyers navigate the market with confidence and avoid integrity risks.

What is a Nationally Determined Contribution (NDC)?

A country’s Nationally Determined Contribution (NDC) is a key element of their commitment to the Paris Agreement. It seeks to embody the efforts of each country to reduce national emissions and adapt to the impacts of climate change. NDCs operationalise the Paris Agreement by turning global climate goals into concrete national actions.

Aotearoa New Zealand’s NDC is to reduce net greenhouse gas (GHG) emissions by 51-55% compared to 2005 levels by 2035. This target:

- is economy-wide,

- covers all sectors and greenhouse gases[1],

- allows for the use offshore mitigation in the future where it is more affordable than domestic alternatives and within the national interest[2].

What is the Voluntary Carbon Market (VCM)?

The Voluntary Carbon Market (VCM) is a decentralised market which allows for the sale and purchase of carbon credits generated by projects that have been independently certified as having reduced or removed GHG emissions beyond business as usual[3].

In Aotearoa New Zealand:

- individuals, businesses and organisations can purchase VCM credits,

- the VCM is entirely separated from the regulated Emissions Trading Scheme (ETS),

- the government does not regulate the VCM,

- assurance and issuance of VCM carbon credits relies on independent third-party assessments against recognised international standards.

The interaction and alignment between NDC and VCM

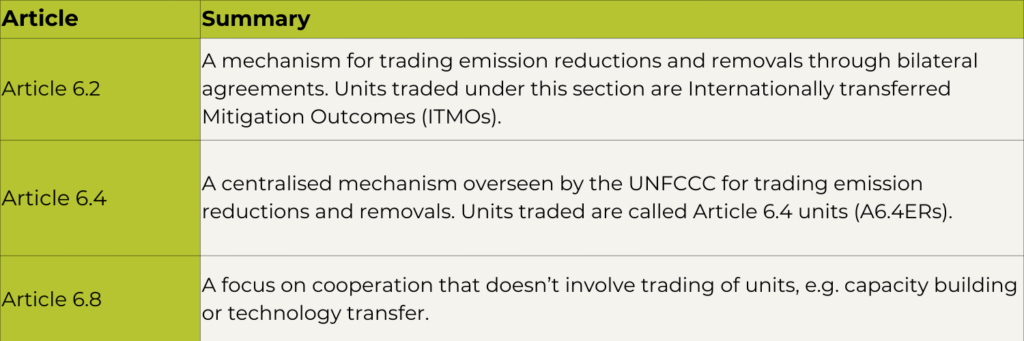

Article 6 of the Paris Agreement

Article 6 of the Paris agreement sets out the rules for international cooperation on climate action and creates mechanisms to allow countries to work together to achieve their NDCs.

The table below summarises the three main articles:

Relationship Between Article 6 Mechanisms and the VCM

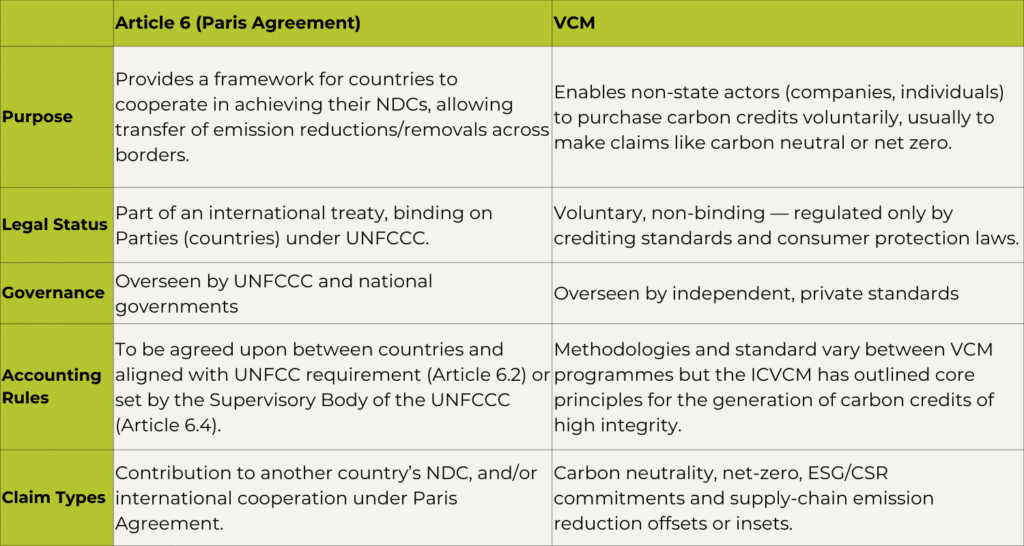

Although both Article 6.2 and 6.4, and the VCM generate credits from emission reduction/removal projects, they are distinct and separate mechanisms.

Article 6-based credits are authorised by governments for use in meeting NDCs, while

VCM credits are primarily for voluntary claims.

Both systems have different accounting requirements, separate governance structures and cater to different end-users.

An NDC target is not the same as participating in VCM, and the VCM is not considered a replacement for robust policy action.

However, there are opportunities for VCM credits to be included within a countries NDC. High integrity VCM initiatives, such as those aligned with Integrity Council for the VCM’s (ICVCM) Core Carbon Principles (CCPs), can be designed to align with Article 6 requirements.

CCP tagged VCM credits can be traded between countries as ITMOs under Article 6.2, but this requires authorisation from the host country and for the host country to have a bilateral agreement for this trade with a buyer country.

Existing VCM credits are not eligible to transition into A6.4ERs, but project developers will be able to follow the standards and guidance developed by the Article 6.4 Supervisory Body to develop new projects which can generate these A6.4ERs.

Similar to ITMOs, for a project developer to sell A6.4ERs to another country for use towards their NDC the host country must provide authorisation for the trade to take place.

The table below outlines the key differences between the VCM and Article 6 which governs a country’s NDC.

What about ‘Double Counting’?

Double counting occurs when GHG emission reductions or removals are accounted for more than once, towards different GHG mitigation targets or claims.

Avoiding Double Counting Under Article 6

Under Article 6.2 double counting is avoided because:

host countries must apply a corresponding adjustment[2] when authorising ITMO transfers,

this removes the transferred emissions reductions/removals from their NDC,

the acquiring country counts the ITMO toward its own NDC,

therefore, the same mitigation cannot be counted twice.

For Article 6.4, the risk of double claiming is restricted to situations where the transferred emissions reductions or removals (AR6.4s) are included in the scope of the host country’s NDC. Where this is the case:

a corresponding adjustment is unequivocally required for the authorization and transfer of AR6.4s.

If the AR6.4s traded are outside of the host country’s NDC, double claiming will not be an issue and a corresponding adjustment is not required.

Double Counting Between NDCs and Corporate Claims

The UNFCCC does not consider the potential for double counting between NDCs and corporate voluntary carbon claims. Therefore:

Credits included in a country’s NDC that are also claimed by a corporate entity do not require a corresponding adjustment.

Companies must undertake their own due diligence if they wish to ensure their claims are not associated with an NDC.

Should VCM Credits have a corresponding Adjustment?

Some stakeholders in the VCM see voluntary credits that are backed by a corresponding adjustment as having higher integrity and want to buy carbon credits which are not included within a host countries NDC.

However, experts have warned this approach could lead countries to make corresponding adjustments available to encourage foreign investment in private VCM activities, but VCM activities may already fall outside the host country’s NDC.

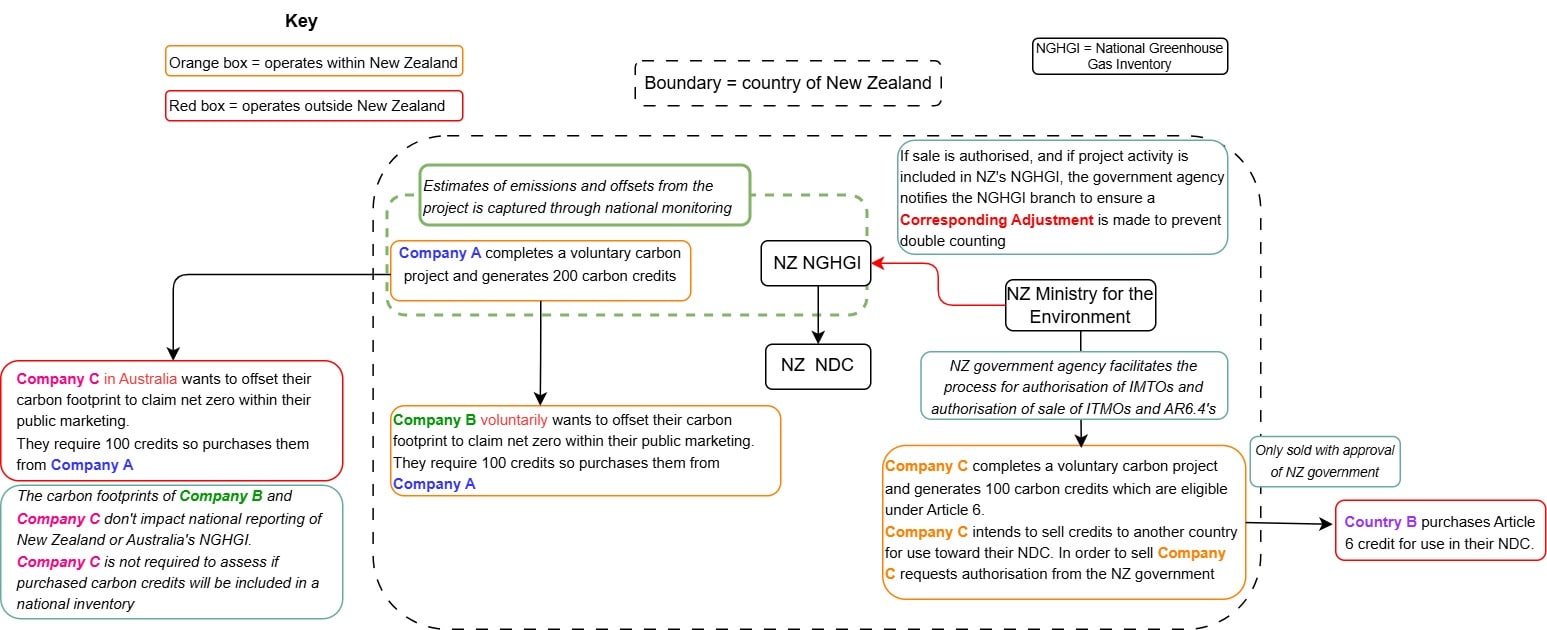

For example, if carbon credits from a NZ-based project are sold through the VCM to a company operating in Australia. The company purchasing the credits can use the NZ-based carbon credits to offset their carbon footprint and make carbon related claims through their marketing. However, the offset claimed by the company will not be included in Australia’s NDC, and will remain in NZ’s NDC. Therefore, there is no impact from a NDC reporting standpoint. If the company is concerned about the double counting between New Zealand’s NDC and their corporate claim they may seek to buy alternative credits which are outside of the host countries NDC but it would be the companies responsibility to undertake this due diligence.

There are ongoing discussions to continue the alignment of VCM projects and NDCs to ensure voluntary actions can contribute to global climate goals without creating double counting issues.

The separation between VCM activity and NDCs (diagram).

References

[1] “Nationally Determined Contribution,” Ministry for the Environment. Accessed: July 16, 2025. [Online]. Available: https://environment.govt.nz/what-government-is-doing/areas-of-work/climate-change/nationally-determined-contribution/

[2] Climate Focus, “The Voluntary Carbon Market Explained.” VCMPrimer, 2021. [Online]. Available: https://climatefocus.com/wp-content/uploads/2021/12/20230118_VCM-Explained_All-Chapters_Compressed_final.pdf

[3] The Integrity Council for the Voluntary Carbon Market, “The Voluntary Carbon Market Explained,” The Voluntary Carbon Market Explained. Accessed: July 16, 2025. [Online]. Available: https://icvcm.org/voluntary-carbon-market-explained/