As scrutiny of the environmental impacts entities have across their entire value chains increase globally, especially for those in the agricultural sector, the Greenhouse Gas Protocol has released additional guidance and standards to support improved emission estimation and reporting of Scope 3 emissions (in their Corporate Value Chain (Scope 3) Accounting and Reporting Standard [1] and its supplementary Technical Guidance [2]), as well as for emissions and removals occurring from land-based activities (in their draft Land Sector and Removals Guidance (LSRG) [3] and the sector-specific Agricultural Guidance [4]).

Each of these standards lists what must be disclosed in GHG inventory reports by entities wanting to conform with the GHG Protocol Standard [5]. This includes a combination of quantitative information (for example, emissions data) and qualitative information (for example, a description of the inventory quality).

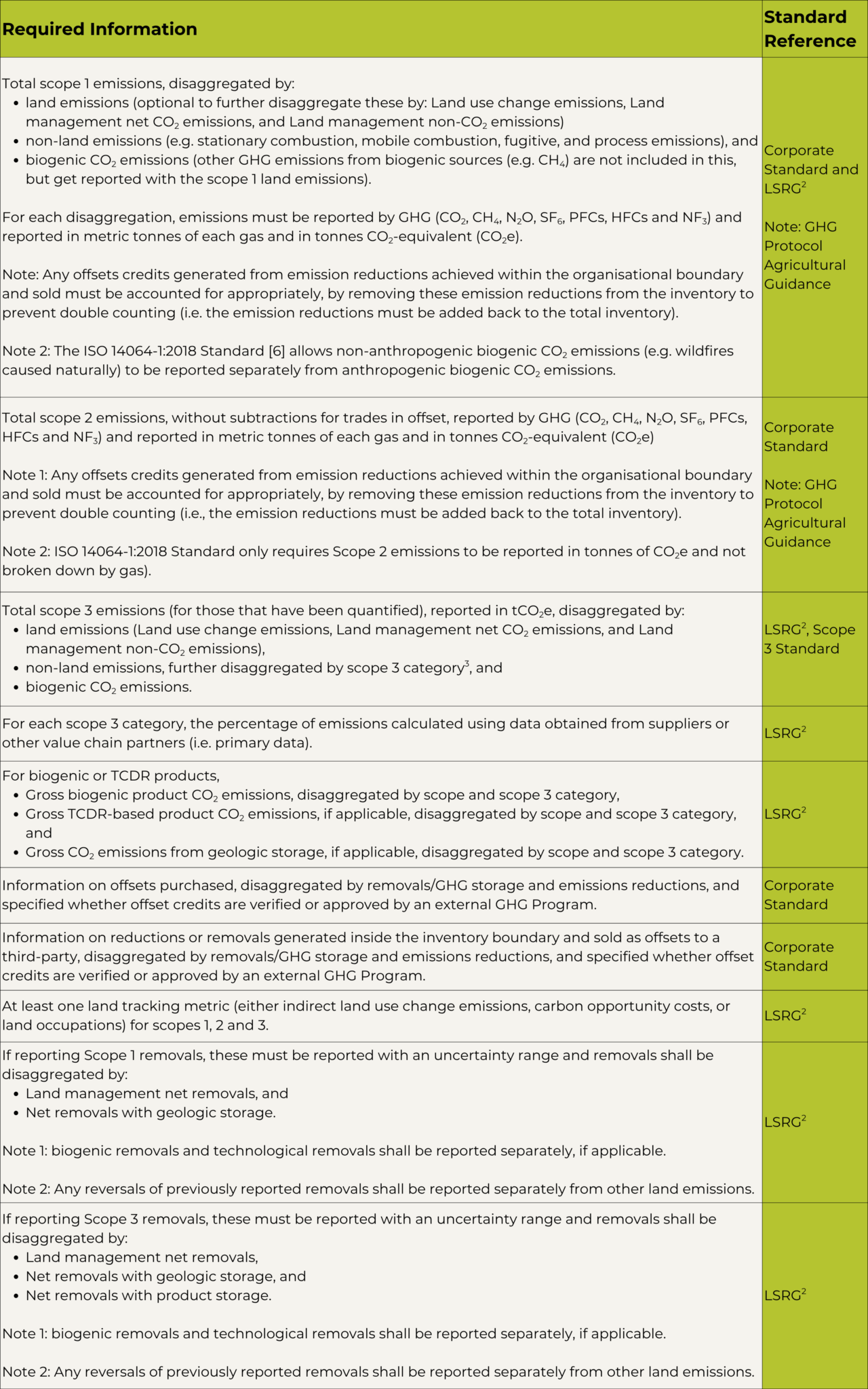

We have compiled a list of the required quantitative information1 for FLAG-sector entities to report on. The following quantitative information regarding emissions and removals must be reported by entities wanting to conform with the GHG Protocol for corporate- or organisation-level GHG inventory reporting, if the entity has land sector activities in its operations or value chain or if the company is reporting removals.

The Greenhouse Gas Protocol standards and guidance are subject to regular reviews, which may lead to changes. These updates aim to align with best practice to ensure the Greenhouse Gas Protocol provides a credible basis [7]. It is important to remain aware of the latest versions of the relevant guidance and standards.

1It is worth noting that the standards list additional optional information that is recommended to report to improve transparency and completeness of the inventory reports. Such information has not been included in our summary.

2It is important to note that the LSRG is still in draft form.

3Scope 3 categories are:

- Purchased goods and services

- Capital goods

- Fuel- and energy-related activities (not included in scope 1 or scope 2)

- Upstream transportation and distribution

- Waste generated in operations

- Business travel

- Employee commuting

- Upstream leased assets

- Downstream transportation and distribution

- Processing of sold products

- Use of sold products

- End-of-life treatment of sold products

- Downstream leased assets

- Franchises

- Investments

References:

[1] World Business Council for Sustainable Development (WBCSD) and World Resources Institute (WRI), (2011), Greenhouse Gas Protocol “Corporate Value Chain (Scope 3) Accounting and Reporting Standard Supplement to the GHG Protocol Corporate Accounting and Reporting Standard”, WBCSD and WRI. https://ghgprotocol.org/corporate-value-chain-scope-3-standard

[2] World Business Council for Sustainable Development (WBCSD) and World Resources Institute (WRI), (2013), Greenhouse Gas Protocol, “Technical Guidance for Calculating Scope 3 Emissions Supplement to the Corporate Value Chain (Scope 3) Accounting & Reporting Standard version 1.0”, WBCSD and WRI. https://ghgprotocol.org/scope-3-calculation-guidance-2

[3] World Business Council for Sustainable Development (WBCSD) and World Resources Institute (WRI), Greenhouse Gas Protocol, (2024), “Land Sector and Removals Initiative”, WBCSD and WRI. https://ghgprotocol.org/land-sector-and-removals-guidance

[4] World Business Council for Sustainable Development (WBCSD)and World Resources Institute (WRI), (2014), Greenhouse Gas Protocol, “Agricultural Guidance Interpreting the Corporate Accounting and Reporting Standard for the agricultural sector”, WBCSD and WRI. https://ghgprotocol.org/agriculture-guidance

[5] World Business Council for Sustainable Development (WBCSD) and World Resources Institute (WRI), (2004) The Greenhouse Gas Protocol, “A Corporate Accounting and Reporting Standard Revised Edition”, WBCSD and WRI. https://ghgprotocol.org/corporate-standard

[6] International Organization for Standardization (ISO), (2018) “Greenhouse gases – Part 1: Specification with guidance at the organization level for quantification and reporting of greenhouse gas emissions and removals”, (ISO Standard No. 14064-1:2018). https://www.iso.org/standard/66453.html

[7] World Business Council for Sustainable Development (WBCSD) and World Resources Institute (WRI), “GHG Protocol Corporate Suite of Standards and Guidance Update Process”, WBCSD and WRI. https://ghgprotocol.org/ghg-protocol-corporate-suite-standards-and-guidance-update-process